With the commercialization of innovations like blockchain, machine learning (ML), and open API, the insurance industry is facing a complete overhaul of the traditional business model. The responsibilities of brokers and underwriters are being increasingly automated, and value is shifting towards consumers and companies embracing these new technologies.

First let’s take a look at the traditional value chain:

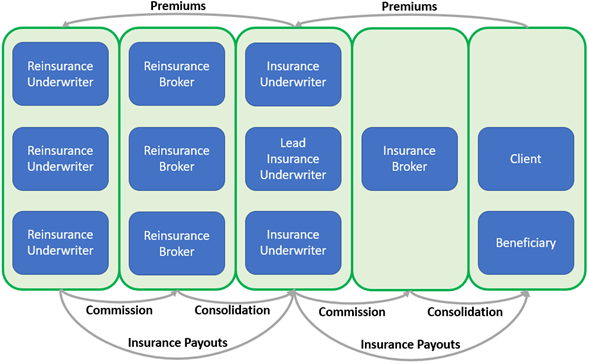

The figure above shows the basic insurance value chain that has existed for hundreds of years:

- Clients will work with a broker to assess their insurance needs

- The broker will work with one or more underwriters to assess risk of the client

- The underwriter(s) will determine a premium that is proportional to the level of risk

- The broker will consolidate this information and provide a quote to the client

- The broker will take a commission, and continue to manage the client relationship

- Underwriters will often pay premiums to reinsurers to spread risk

Despite the endurance of this value chain, it contains three primary flaws:

- High costs due to many intermediaries taking a cut of the premiums

- Misaligned incentives between insurers, brokers, and clients

- Long wait times and low transparency

With so much inefficiency, incumbents in the industry are facing an ultimatum to change or be replaced by the myriad of Fintech startups looking to capture their share of the value. Let’s look at a few ways in which decentralization is addressing these issues.

High costs due to many intermediaries taking a cut of the premiums

Automation in the insurance industry is rendering the traditional roles of brokers and underwriters obsolete. With the world becoming increasingly connected, brokers are no longer needed to educate consumers about their coverage needs and help them bundle products together.

The Singaporean startup PolicyPal has created a platform which directly connects customers with insurers, automating the role of the broker. The platform offers policies from a wide range of insurers, so that consumers are not limited to the specific company that the broker works for. This allows consumers to build their own policies using the products that make sense for them while also reducing their premiums by cutting out the middleman.

Incumbents are also investing in technology to reduce their dependency on human labor. TD has developed their own application called TD MyAdvantage which tracks driving habits and offers discounts based on safe behavior. Other companies like the American startup Root is taking this a step further, by using driving habits as a primary predictor of risk. These applications are automating the role of insurance adjusters, shifting value back to consumers by offering lower premiums, and helping create safer roads.

Misaligned incentives between insurers, brokers, and clients

In a typical insurer-client relationship, the incentives between the two parties are aligned until something goes wrong. For example, in an auto-insurance contract, both the client and insurer want to prevent an accident. However, as soon as an accident occurs, the insurer will attempt to minimize their payouts, while the client simply wants to get their car fixed and paid for.

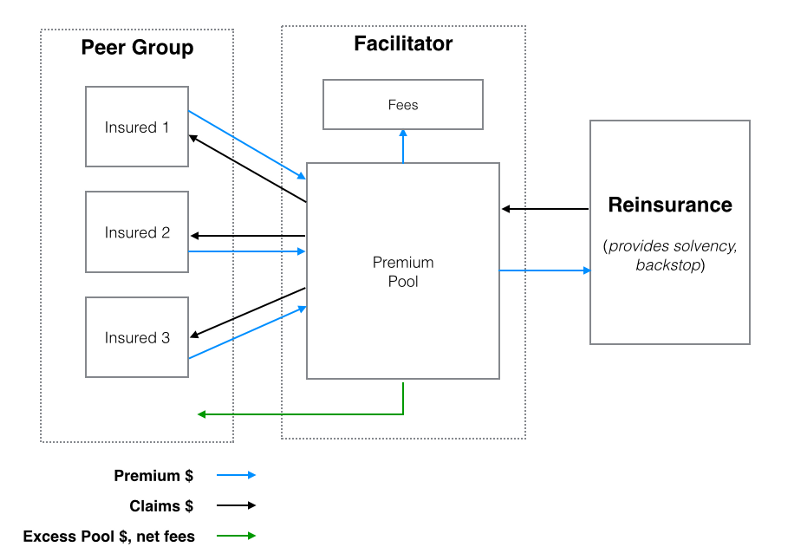

Peer-to-peer (P2P) insurance has become an increasingly popular way to address this issue by operating on the simple and timeless principle of ‘treat others as you’d like to be treated’. For example, the Chinese platform TongJuBao allows community members to buy into a P2P insurance plan and set their coverage details as a group without the influence of a third profit-seeking party. The company charges a small service fee, but the premiums that are unpaid at the end of each period are returned to the community members, removing any incentives for not paying out claims. The below figure shows a basic operating model for a P2P insurance platform.

To reduce consumer mistrust in human brokers, companies are also developing more sophisticated needs assessment tools to provide consumers with less biased information on their insurance needs. For example, Manulife has created the InsureRight Calculator, their own needs assessment tool which allows prospective customers to get a recommendation of the coverage that best suits them based on their personal situation, and connect them directly to the insurer to finalize their policy. These innovations push the value in both directions, with insurers saving money on labor and customers enjoying more competitive prices due to lower administrative costs.

Long wait times and low transparency

With the continued increase in availability and timeliness of data, it is now possible to execute payouts using smart contracts based on automated assessment of the claim using available data. For example, Etherisc is a startup that is piloting a flight insurance offering using smart contracts. Customers will be automatically paid out when their flight is cancelled because the cancellation is public data that can be tracked through the smart contract. This same application can be applied to property insurance (using satellite imagery or police reports), auto insurance (using dashcam footage), and life/health insurance (using medical records). Some data such as satellite imagery are easier to obtain than others, but the savings from reducing claims assessment and payout wait times will often justify the integration with these new sources of data.

Insurance companies can also increase transparency by applying blockchain towards records of insurance transaction and claims history. With a shared ledger across the value chain, many steps related to data verification and document sharing can be cut out of the claims process. When the insured, the insurer, the reinsurer, and other relevant 3rd parties all agree on the content of the coverage and details of the claim, significantly less time and resources are wasted on data validation and claim disputes across parties.

Barriers to Innovation

Regulations in the insurance industry are the biggest barriers to innovation, due to differing regulatory frameworks across regions. In Canada, every province has different regulatory standards for insurers, and new products/services must cater to these standards across all provinces. Additionally, requirements for burdensome compliance reporting and restrictions on data flow have led to grey areas when it comes to implementing new technologies like blockchain, discouraging companies big and small from testing out novel applications for these innovations.

Another barrier for innovation within large insurers is the continued usage of legacy technologies and processes. While most insurers have digitized their data and claims processes, these processes still require significant manual intervention. For example, making adjustments to insurance policies still requires customers to speak with a broker, which impedes quality and consistency in customer experience compared to fully digitized Fintech startups. Developing these digital capabilities will be costly to large national insurers, but the risks of falling behind with adoption of customer-centric innovations can be a stronger driving force for change.